By David S. Bauders, CEO SPARXiQ

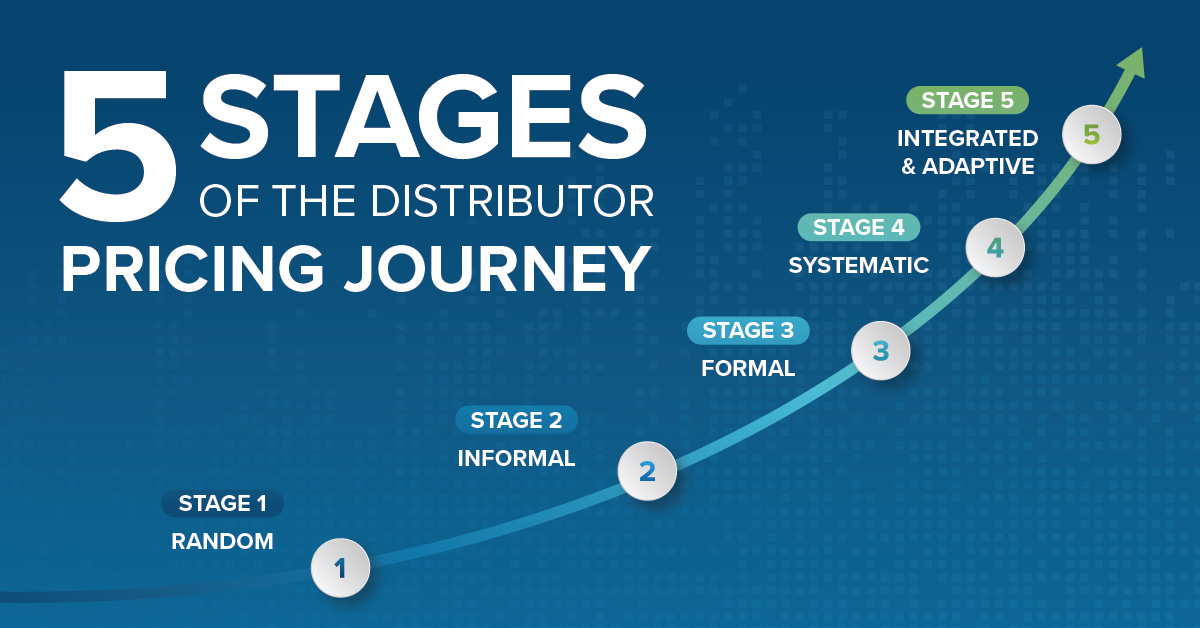

Every distributor is on a strategic pricing journey. The fundamental pricing challenge — thousands of SKUs, thousands of customers, and seller-negotiated pricing — is virtually endemic to distribution. Every day, quote by quote, decisions are made that determine the net profitability and organic growth rate of distributors. Everyone is working the same number of hours, but the value captured by each distributor depends on how this core business process is executed. Typically, distributors can capture 100 basis points or more from each stage progression, totaling 500 basis points or more.

Stage Zero: The Wild West Approach to Pricing

The default state for the vast majority of distributors is a “Wild West” approach to pricing. They often price using peanut-butter margins ending in 0s and 5s or gravitate towards the nifty Last Price Paid feature in their ERP system. Companies in this stage tend to adhere to the mantra of “Leave Them Alone and Let Them Sell,” assuming their sellers understand market pricing. This approach, lacking tools, training, and processes, leads companies to perform at the bottom of industry profitability and growth metrics. Until these companies move up the maturity ladder, they risk being acquired by others who have advanced further.

Stage 1: Random Pricing

The first stage in the pricing maturity model is Random Pricing, which really describes an inconsistent use of structured pricing. In this stage, someone has started to implement some pricing matrices to offer sellers a simpler, more consistent or superficially logical approach to pricing. Often built in home-grown Excel spreadsheets, these pricing matrices are oversimplified and heavily based on cost-plus approaches, as in the Wild West state. Here, pricing matrices at least attempt to relate margin levels with customer segment, size or geography, and often differentiate by vendor or product family. However, as these companies’ pricing recommendations stem from internally derived, anecdotal, cost-based assessments of appropriate margins – rather than the true drivers of market pricing and share-acquisition — the adoption of these matrices is predictably poor, as is their alignment with market-level pricing expectations. Pricing overrides to these primitive systems can account for 50 percent or more of transactions.

Stage 2: Informal Pricing

With a bit of a foundation in place from Stage One, companies that progress in their journey work to get the most out of their existing pricing spreadsheets. While many distributors are still uneasy about transitioning to a formal pricing initiative in this stage, which requires a focus on change management, they acknowledge the value in refining their existing practices.

Companies progressing to Stage Two aim to refine their pricing spreadsheets to identify areas that can support price premiums. In addition to moving towards market-level pricing for commonly sold product categories, they’ll attack various areas of their pricing methods mix, based on existing pricing habits to find the easiest areas for improvement while minimizing pushback from the sales team or customers.

Stage 3: Formal Pricing

In Stage 3, companies strategically price based on market sensitivity, moving beyond simplistic Excel spreadsheets to dynamic, adaptive pricing algorithms that address customer share-of-wallet and price sensitivity. They systematically review and optimize contracts and CSPs, pruning unprofitable customers or customer/product combinations and enhancing those needed to support sales objectives.

Stage 4: Systematic Pricing

After reaching the formal maturity in Stage Three, companies can further improve by implementing systems, tools, policies, training and incentives to augment the analytically driven systems already in place. The goal is to facilitate adjustments in the sales team’s behavior that align the strategic pricing initiative with the sales-growth objectives.

Among other policy and process standards, Stage Four companies establish eligibility requirements around overrides, as well as pricing “bands” and “floors” that control the range of overrides. Doing so provides field flexibility to address daily market realities while controlling the magnitude of override margin leakage. To be most effective in daily workflow, these rules and “guardrails” must be integrated directly into ERP and/or CRM order entry. Properly implemented, with supporting training and incentives, price bands provide an appropriate blend of flexibility and control, thus helping to resolve the Top-Line versus Bottom-Line debate.

Stage 5: Integrated & Adaptive Pricing

For companies that have optimized pricing at Stage Four, the next potential progression is to Stage Five where pricing is further refined by integrating and adapting sales performance, vendor cost of goods sold (COGS) and customer-level cost-to-serve.

In Stage Five, sellers progress into data-driven, optimized Strategic Account Management. Strategic Account Management requires sellers to consistently and holistically manage the full dynamics of customer profitability across four key interdependent levers: pricing, sales mix and share of customer wallet, vendor product COGS, and customer cost-to-serve.

Companies that master and sustain Stage Five of this process outperform their peers by 400 to

800 basis points or more ($4 million to $8 million per year per $100 million in revenue), accumulating more capital to invest in growth as well as capabilities to support acquisition of their lesser competitors. Distributors who attain and sustain pricing mastery outperform industry average profitability by 50 to 200 percent or more.

They can invest in value-creation and competitive capabilities to drive organic growth. They also can accelerate inorganic growth by predictably profiting from arbitrage opportunities via acquisitions: buying books of business of distributors less evolved in their pricing capabilities. They are better for their customers, vendors, employees and shareholders, and tougher for their competitors. They are platform businesses positioned to attract and reward capital and to shape the markets of the future.