By David S. Bauders, CEO SPARXiQ

Especially in the new tariff economy, with an unprecedented velocity and magnitude of cost increases, distributors need to get their pricing houses in order. While the tariff impact on distributors varies widely and daily, I’d like to share some of the common risks that tariffs can inflict on distributors generally. Cumulatively, when not carefully managed, they can reduce Peak Internal Profitability from 12 percent EBITDA or more down to the meager 4 percent average that plagues the distribution industry — destroying up to two-thirds of peak value added.

The root cause of the toxic follies that follow is Wild West Pricing: the natural state of selling where outside and inside salespeople are the real price setters in the organization. For many sellers, they believe setting (guessing) prices is a core part of their job. That is, since they are closest to the customer, they best “know where their customers need them to be.”

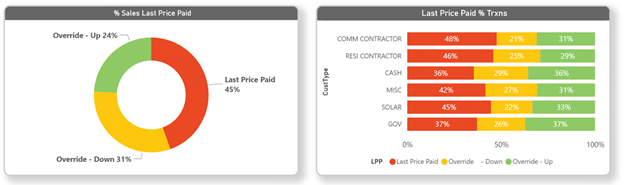

Last Price Paid

With all the inflation since COVID and the pending impact of tariffs, it’s surprising how many distributor sales transactions are priced using Last Price Paid (LPP) logic. In this case, the ERP system is insidiously abetting Wild West Pricing by automating the process of identifying the last price a particular customer paid for a product — or even the last price any customer paid for that product. Beyond the dubious assumption that a customer needs every price to be the same from order to order, there is the obvious issue of whether the cost basis has changed since the last time it was ordered. In addition, LPP will repeat and compound earlier pricing errors.

In general, we see 20 percent or more of Wild West distributors’ pricing coming from LPP, with an average leakage value of 500 to 1,000 basis points on affected revenue. That translates to a loss of 100 basis points on overall revenue, or 25% of the average distributor’s operating profit.

Pricing Overrides

In the Wild West pricing paradigm, pricing overrides are a feature, not a bug, of how pricing works. Since the sales team “knows the market” better than anyone else, its job is to adjust pricing away from system pricing. That is, overriding system pricing is their job. Despite the fact that customers rarely know the distributor’s cost, the salespeople often apply Cost Plus techniques, usually choosing low numbers that end in 0s and 5s. Disturbingly, sellers will even override system pricing on rush orders, high-cost-to-serve, long-tail products, proprietary products, and even known one-off orders.

With 20 to 50 percent of revenue coming from overrides, and at a margin delta of 500 to 1,000 basis points versus system pricing, the average distributor is forfeiting 100 to 500 basis points on overall revenues, or 25% to 125% of the average distributor’s operating profit.

Set It & Forget It Contract/CSP Pricing

While we can all recognize the competitive intensity of large projects, annual-spend contracts, and customer-specific pricing agreements (CSP), a cardinal sin of market laggards is setting and forgetting such pricing for prolonged periods of time. Obviously, expressing such long-term agreements as net prices shifts all the inflationary and tariff risk to the distributor. Also, the same sellers who so eagerly and prodigiously set up these agreements lack the motivation or tools to systematically identify and remediate defects in a timely manner. Many throw in the towel and set the expiration date to 12/31/2099 (!) — or just roll it over year after year.

A properly structured contract or CSP features carefully delineated, declared pricing on Planned Spend, while preserving “price on request” for unplanned spending. Aggressively pricing on Planned Spend (supported rigorously by vendor cost supports) is balanced by offsetting, non-declared, premium pricing on Unplanned Spend.

Like Pricing Overrides above, Contracts/CSP carry margins 500 to 1,000 basis points below system pricing. Commonly constituting 20 to 40 percent or more of revenues, when Contract/CSP pricing is misused, overused, or perpetuated beyond their competitive relevancy date, they sacrifice operating profits by 100 to 400 basis points, or 25 to 100 percent of the average distributor’s operating profits.

Peanut Butter Pricing & Broken Product Families

Not only does the Wild West seller tend to use margins with 0s and 5s, they also apply them in a peanut-butter fashion to all SKUs in a given product family (or even on all families in a bill of materials). Because long-tail SKUs in these families tend to be more costly to serve and be less price-sensitive to the customer, peanut butter pricing produces much of the profit leakage in pricing. This means that many such SKUs are actually money-losing at the net profit level.

Lacking an appropriate SKU-level pricing differentiation within their product families, the average distributor sacrifices additional 200 to 400 basis points on up to 30 percent of their system pricing, or up to 60 to 120 basis points on overall revenue — which represents 15 to 30 percent of overall average profitability.

Free to Choose

The path to mediocre profitability is not hard to achieve. All that’s really required is an unshakeable belief in, unawareness of, or failure to overturn, the folly of Wild West selling and pricing. In today’s dynamic and tariff-facing economy, distributors who fail to choose to overturn the reign of Wild West selling will naturally be acquired by those who do. Efficient markets will create arbitrage opportunities for those who overturn the stubborn reign of foolishness and set themselves on the path of rigorous, systematic pricing.

With the growing role of artificial intelligence in pricing tools, the stubborn reign of foolish Wild West pricing is rapidly breaking down. Simply put, lone sellers can’t match the sophistication and accuracy of price optimization systems. Tariff pressures will finally push the arbitrage question to the forefront of distributor survival. As always, change creates winners and losers.