By: David S. Bauders, CEO SPARXiQ: Intelligent Sales and Profit Acceleration

Inflation, stagnation, recession — recent economic signals have suggested a potential shift away from the heady economy enjoyed in the rebound from pandemic lockdowns. Due to a number of factors affecting the economy, such as rising oil and raw material prices, interest rate increases, and resulting stock market declines, the business outlook has become significantly more cautious, if not adverse.

As a result, forward-looking distributors are planning for a potential shift in the business environment. In simple terms, they are trying to lock in and/or future-proof their recent productivity and profitability.

Let’s Look at the Possibility of Stagflation

While no one has a crystal ball, there are a few likely economic scenarios, each with its own distinct challenges:

- Stagflation: a period of stagnant economic growth combined with high inflation and high unemployment.

- Recession: a period during which the economy shrinks; it is commonly defined as two successive quarters of declining gross domestic product (GDP).

- Inflationary Recession: a period of continuing high inflation in which the economy also shrinks (potentially due to supply-side constraints, such as labor or materials), though with low unemployment (potentially due to declining labor force participation rates).

One of the challenges in this economic cycle is navigating the potential for stagflation. In traditional recessions, falling demand and rising unemployment produce stabilizing or falling prices. In the current cycle, there are several important forces that are different:

- Inflation is high, despite aggressive monetary intervention.

- Unemployment is low, despite an economic slowdown (declining labor force participation rate).

- Corporate profitability is up (for now), despite rising costs.

How Stagflation Affects Distributors

It is helpful for distributors to consider the diverse causes of inflation. In today’s economy, four key forces are driving extraordinary inflation:

- Structural/Supply Chain: changes to the supply of goods versus prior state: new frictions in international trade, shifts in energy sources, regulatory environment, war, logistics/shipping, incentives to work, save or invest

- Structural/Demand: changes to the demand for goods versus prior state: shifting preferences for goods (at home) over experiences/service (travel, restaurants)

- Monetary: Central bank (Federal Reserve) supply of cash and equivalents relative to the supply of goods in the economy

- Fiscal: Government taxing & spending policies that increase demand forces faster than supply forces

For distributors, today’s rampant inflation — levels not seen in 40 years — and the Federal Reserve’s response to it (interest rate hikes) is likely to slow economic growth. Because the Federal Reserve is using monetary policy to address inflation that is partially structural in nature, it is likely to either overstep and cause a recession or fail to mitigate the structural inflationary pressures outside of the monetary and fiscal realms. A likely outcome is persistent inflation along with either a stagnant economy or perhaps a recession.

What does that mean for distributors? First, they will continue to have an increasing velocity and magnitude of vendor cost increases. This part is not new anymore, though many are still struggling to fully and timely capture vendor cost increases. What is new is trying to pass through vendor cost increases in a market where competitive intensity for a shrinking pie creates greater price pressure (and concessions/pricing overrides by sales reps to customers). This is the root cause of a stagflation margin squeeze.

Strategic Pricing Mastery Can Outpace Inflation in a Stagnant Economy

At the micro level, if we consider the typical customer market basket, what tends to happen in a shrinking-pie economy is the core products (where the customer is most-price sensitive) experience increased competitive pressure, resulting in lower prices. This happens despite increasing, inflation-based vendor costs. To maintain or grow customer share of wallet, sellers need to sharpen their pricing to provide deeper discounts on only a carefully selected basket of core products, while extracting compensating premiums on non-core products.

The careful and accurate application of these discounts and premiums is critical. Cost-plus, monotonous discounting across products of diverse sensitivity will not be competitive enough on core products and will sacrifice margin premiums on non-core products. Share of wallet and/or margins will decline for companies who fail to master this dynamic as they compete with those who have mastered strategic pricing.

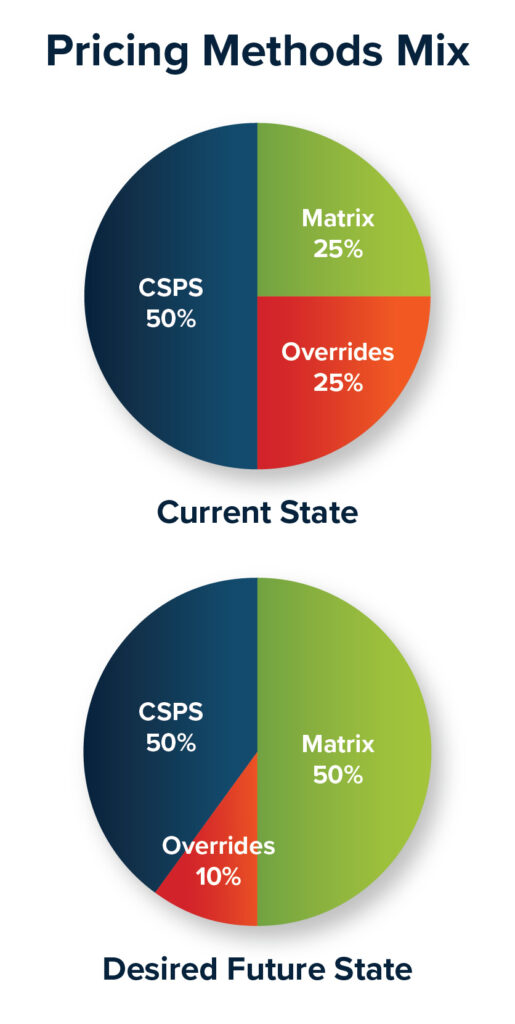

At the macro level, these pressures manifest in the pricing methods mix. For distributors with undisciplined pricing, overrides and overuse of customer-specific pricing (CSP) will increase. As each method carries lower margins than matrix/system pricing, share gains in these methods will drive down overall margins. For distributors without good pricing tools or processes to focus discounting on high-sensitivity items and fence off tail-spend for margin premiums, an adverse pricing method mix will slice their EBITDA significantly.

For example, if overrides carry margins 1,000 basis points (10 margin points) lower than matrix pricing, an increase from 30 percent overrides (as a share of revenue) to 50 percent yields an overall margin decrease of 200 basis points (1,000 basis points x 20 percentage-point increase in overrides). Similarly, if margins in the CSP files decline by 500 basis points due to competitive pressure, and CSP is 30 percent of revenue, the loss is 150 basis points. For the average distributor, having a four percent EBITDA, the combined losses of 350 basis points can nearly eliminate profitability.

Distributors Must Grow Margins to Sustain Profitability

As we are seeing now, inflation is accelerating not only vendor costs, but also the operating costs of running a distribution business. Labor costs, such as attracting and retaining talent, are up. Freight costs have doubled. Energy costs have skyrocketed. In the approaching economy, a distributor will have to grow their gross margins and/or accelerate their productivity further to sustain recent peak profitability.

A typical distributor may have had 30 percent gross margins, 26 percent operating costs, and EBIT of four percent. In our 30/26/4 example, if operating costs rise by 8 percent, the distributor’s gross margins will need to rise from 26 percent to 28.08 percent to simply maintain profitability. Increased competitive pressure from a shrinking-pie economy will undoubtedly require new pricing, purchasing and contracting disciplines. Automating customer ordering can provide both reduced cost-to-serve and pricing consistency to minimize overrides. Vendor rebate optimization can yield additional contributions.

Standing still is not an option in a stagflation economy. No one knows what the future may bring, but smart distributors are investing now to bring new tools, training and technologies to future-proof their businesses Now is the right time to master strategic pricing.